Insurance companies routinely deny NYC buildings with subsidized tenants

July 25, 2023, 5 a.m.

Insurers regularly ask property owners if they rent to tenants with housing vouchers and deny coverage based on their answers. That may be illegal, regulators say.

- heading

- Key findings of Gothamist's investigation

- image

- image

- None

- caption

- body

- It is illegal for landlords in NYC to refuse renting to a tenant because they use a housing voucher. But there is no explicit law that prohibits insurance companies from asking about subsidies or denying a landlord coverage because a building has subsidized units.

- We reviewed 70 property and liability insurance applications and found all but five ask property owners if they rent to tenants who use housing subsidies. We also found examples of companies outright refusing to cover housing where renters pay with vouchers, including Section 8.

- Landlords, insurance brokers and regulators say this practice drives up costs that can get passed down to tenants or cut back on necessary repairs and maintenance.

New York law prevents landlords from discriminating against low-income tenants with rental assistance vouchers, but those same measures don’t apply to insurance companies that routinely refuse to cover buildings that house subsidized tenants.

Dozens of insurance carriers doing business in New York explicitly ask about, and decline to cover, buildings where low-income tenants pay for apartments with housing vouchers, according to a Gothamist review of applications, denials and interviews with insurance brokers, landlords and government regulators.

The practice is now raising concerns among state and federal insurance regulators, and the New York Attorney General's office, that insurers may be unfairly discriminating against groups protected by state and federal fair housing laws. Advocates argue it’s also undermining the city’s efforts to provide affordable housing at a time of rising rents and increasing homelessness and that rules intended to curb insurance discrimination remain weak.

For property owners, the rejections can set off a scramble for coverage, forcing them to pay thousands of dollars more to insure their buildings — costs they either pass on to tenants, or offset by foregoing building maintenance, repairs and other investments. At worst, the practice discourages owners from accepting tenants with rent vouchers, fair housing advocates say.

“Engage in discriminatory practice in order to comply with these policies and receive insurance coverage and lower premiums, or don't engage in discriminatory conduct and be denied the insurance coverage,” said the National Fair Housing Alliance’s top attorney, Morgan Williams. “That's the choice that the landlord would face.”

Gothamist reviewed 70 property and liability application forms from companies that have operated in or are still providing insurance coverage in New York City, with all but five asking whether building owners rent to tenants using housing subsidies, often with specific reference to the federal Section 8 program. Several insurers set explicit thresholds for the number of subsidized households in buildings they will cover, or outright refuse to insure buildings where any tenants at all use rental assistance.

“I can tell you, on a broad spectrum the insurance carriers do not like them. They do not like Section 8 housing,” said Lynn Ziemak, assistant vice president of Brown & Brown of Garden City, a subsidiary of one of the country’s largest brokerage firms.

Ziemak is one of seven brokers — a role that acts as an intermediary between customers and insurers — who spoke with Gothamist about the carriers’ unwillingness to cover buildings for low-income renters. A disproportionate number of tenants who use housing vouchers are people of color, women and renters with disabilities, which are all protected classes under federal and state law. Section 8 and other subsidies, like New York’s CityFHEPS vouchers, pay the bulk of a recipient’s rent, with the tenant contributing 30% of their income each month.

A total of 682 property and liability insurance carriers certified in New York provided coverage in the state last year, according to the Department of Financial Services, or DFS. But just a tiny fraction of those companies agree to insure buildings with subsidized tenants, said Susan Camerata, the chief financial officer of Wavecrest, speaking last week at a panel discussion in Manhattan on rising insurance rates. Wavecrest owns or manages 30,000 apartments in New York.

“It’s really a major problem,” Camerata said. “We specialize in affordable housing. That’s who our clients are. So why is it that building being segregated, or my word, ‘redlined,’ because there’s Section 8 in the building?” Camerata said.

So-called “source of income discrimination” is often considered a proxy for other forms of bias, including against people based on their race, religion, familial status, gender, disability or other protected class.

If insurance companies’ questions about housing vouchers have the effect of discriminating against those protected classed, then “housing discrimination in violation of the Fair Housing Act may have occurred,” said Alicka Ampry-Samuel, the New York regional administrator for the federal Department of Housing and Urban Development. The U.S. agency administers the Section 8 program.

“A violation may be intentionally discriminatory or have an unjustified discriminatory effect. For example, if an insurer denies coverage or charges higher rates because housing includes Section 8 residents, and that action discriminates because of one of the protected characteristics, it may violate the Act,” Ampry-Samuel added. “HUD takes violations of the Fair Housing Act seriously.”

In response to questions from Gothamist, DFS said it will begin requesting more detailed information from insurers about how questions related to subsidized housing are used to determine insurance rates and whether coverage is denied.

A spokesperson for Attorney General Letitia James said her office is aware of the practice and is investigating claims from property owners who said they were denied coverage because they rent to tenants with housing vouchers.

Rising insurance costs

Questions about housing subsidies come from major insurance carriers and small local firms alike.

Travelers, a large Manhattan-based insurer, settled a 2016 lawsuit accusing it of explicitly denying coverage for Section 8 housing in Washington D.C. The company continues to ask landlords for the percentage of their units that are “rented as Section 8 or subsidized housing” on its application forms.

The much smaller Manhattan-based firm Brownstone Agency specializes in covering low-rise homes in New York City’s tonier neighborhoods and lists buildings with Section 8 recipients among what it categorizes as “ineligible risks” on its application.

Property owners say refusals by insurers force them to find coverage on a separate market, known as the “the excess and surplus market,” which is not subject to the same level of state oversight and where companies typically set far higher rates.

“It has no bearing whether people are poor; it has to do with risk.”

Loretta Worters, Insurance Information Institute, an industry trade group

A report published late last year by DFS and New York’s Division of Homes and Community Renewal found that insurance premiums increased by an average of 43% between 2019 and 2021 across 20,000 units of affordable and income-restricted housing that the agencies reviewed.

In many cases, that means passing costs onto tenants in the form of higher rents, said University Neighborhood Housing Program’s Director of Real Estate Brendan Mitchell, whose organization owns or oversees around 1,200 apartments and has studied the impact of rising insurance rates.

In buildings with a large number of rent-stabilized apartments, where rents cannot be significantly increased, the rising price of insurance discourages new investment or even repairs, Mitchell said.

“It just means you're foregoing something else,” Mitchell said. “If you're seeing a 30% increase in insurance, the first thing to go is putting solar panels on your roof. The next thing to go is non-emergency repairs.”

Insurance ‘redlining’

Companies that decline to cover subsidized housing for low-income New Yorkers face little accountability, according to landlords and fair housing groups, though regulators said they will begin to monitor the practice more closely.

No rule explicitly prohibits insurance carriers from requesting information from owners about tenants who receive rental vouchers, or declining to cover subsidized or affordable housing if they can demonstrate some commercial reason for the denial.

Two carriers referred questions about their underwriting practices to the Insurance Information Institute, an industry trade group. The group’s spokesperson, Loretta Worters, said insurance carriers do regularly ask if owners rent to people with housing subsidies, but argued that questions about tenant characteristics relate to the physical condition of the property.

“Insurance companies often ask whether buildings contain affordable, subsidized, or Section 8 units, and what proportion of the buildings is comprised of such units, in order to make decisions about which properties to insure and at what price,” Worters said.

“It has no bearing whether people are poor; it has to do with risk,” she added, while also listing “age of building, type of construction, lack of sprinklers or a number of other legitimate factors.”

She did not respond to a question about how subsidized tenants pose similar risks to the physical characteristics of a building.

In recent years, fair housing groups in Washington D.C., New Orleans and other parts of the country have sued carriers over the practice and reached financial settlements. California law prohibits insurance carriers from asking whether tenants have rental subsidies.

The National Fair Housing Alliance won a settlement from Travelers after suing the company for using what it called “discriminatory underwriting and eligibility criteria” around Section 8 housing with a disparate impact on Black families and households headed by women.

So far, no such enforcement or litigation has taken place in New York.

“There's an anti-redlining statute, but it's extremely weak,” said New York State Association for Affordable Housing Policy Director James Lloyd. “If there’s any commercial reason whatsoever to deny the coverage, then you can deny it or charge more, so the law doesn’t have a lot of teeth.”

The lack of scrutiny has infuriated fair housing advocates who say carriers are using questions about Section 8 to deny coverage for buildings with low-income renters, based on class and racist stereotypes. In New York City, about 47% of Section 8 recipients identify as Black or African American, nearly 40% as Hispanic of Latino, and about half have a disability, according to city data

“It’s making some assumptions about low-income renters that fundamentally seem unfair and unjust,” said New York Housing Conference Executive Director Rachel Fee, whose group has begun organizing landlords against insurance bias. “Essentially it seems like blatant discrimination to even ask how someone is paying their rent and if they’re using a Section 8 voucher. How is that an indication of risk for an insurer? I find that offensive.”

“I’m in disbelief that blatant discrimination of this kind is allowed in a regulated industry,” Fee added.

‘Ineligible risk’

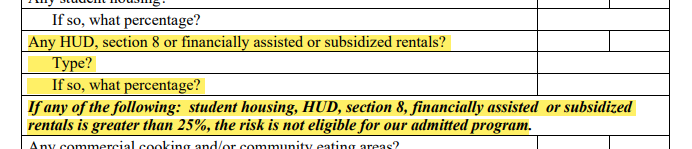

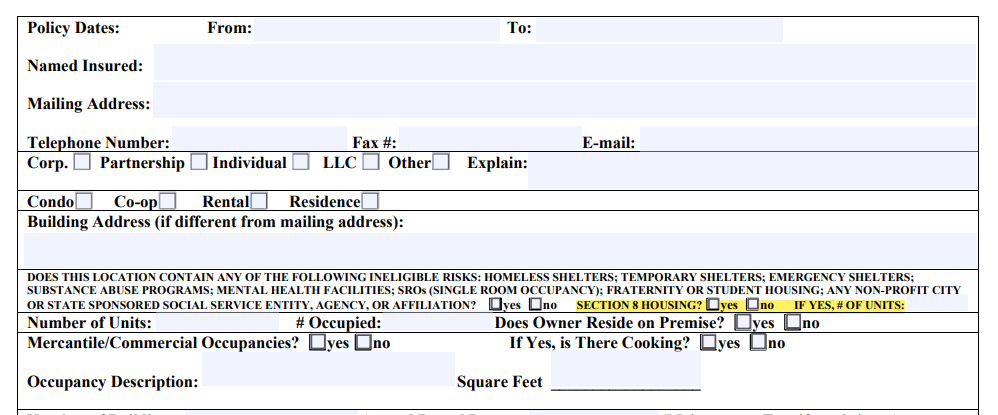

Nearly all of the insurance applications reviewed by Gothamist require owners to list the percentage of units occupied by tenants who use housing vouchers. On two recent underwriting applications from Brownstone Agency, “Section 8 Housing” is grouped with several other categories it considers to be “ineligible risks,” including homeless shelters, bed and breakfasts and student housing — transient accommodations that, unlike housing voucher programs, are not meant to provide permanent housing.

An underwriting application from the insurance firm Program Brokerage Corporation requires owners to answer the question: “Are there any locations having more than 15% subsidized housing?” The query is positioned on the form among requests for information about bed bug infestations, the number of building exits and whether the property has any docks or marinas.

Responses to questions about subsidized housing appear to affect the insurer’s coverage decisions.

When a group of large affordable housing landlords in New York City submitted seven examples of denials based on affordable and subsidized housing to state regulators last year, they included an email from Program Brokerage Corporation noting that it will only cover buildings with “no more than 20%” Section 8 tenants. The Department of Financial Services cited that response in an industry report last year.

Brownstone did not respond to multiple phone calls, emails or a visit to their corporate headquarters in Lower Manhattan. Gary Shapiro, a senior vice president at Program Brokerage Corporation, declined to comment when contacted by phone last month. He and other administrators at the company did not respond to multiple emails asking about the reason for the question.

Applications from the companies Seneca Insurance and Colony Specialty, a subsidiary of the firm Argo, each say they will not cover properties where more than 25% of apartments are subsidized.

Argo spokesperson David Snowden said his company sold most of its property and casualty coverage to another firm in 2021 and declined to comment on past business practices.

Seneca did not respond to emails seeking comment.

Gothamist contacted the 10 largest property and liability carriers in the country, based on market share analysis, and asked about their coverage of subsidized housing in New York City. Only USAA responded, saying it does not cover large multi-family properties at all in the five boroughs. A spokesperson for Nationwide declined to comment, but the company’s 2023 policy guidelines said it does not cover apartment buildings with more than four units in New York City.

Travelers, the subject of multiple fair housing lawsuits elsewhere in the country, did not initially provide comment on the record.

A day after this article was published, a Travelers spokesperson, Kate Thermansen, followed-up with Gothamist to say the company began using an updated insurance application seven years ago that does not include questions related to housing subsidies, though the current application does ask for information on monthly rent amounts. Gothamist obtained applications for Travelers and its subsidiary, Northfield, in recent weeks from two brokerage firms. Those applications, which the firms actively used and pointed potential customers to, contain questions about the number of rent subsidized tenants. Thermansen said Travelers has instructed those brokers to no longer use those forms. She said Travelers does not discriminate against subsidized tenants.

State Farm and Berkshire Hathway, the country’s two largest casualty insurance companies, did not provide a response. But an application for the Berkshire Hathaway subsidiaries, RSUI Group and Devon Park Specialty Insurance, each ask about the number of subsidized apartments in their applications

“If over 15% the risk is not eligible for coverage with RSUI,” one application states.

RSUI also did not respond to emails seeking comment.

Gothamist interviewed 16 landlords — from the heads of companies that own thousands of units, to the owner of a single multi-family building — who said they believe the implications of the questions are clear: Renting units to people with housing vouchers leads to higher premiums, or outright denials.

“They ask about your composition and how many Section 8 tenants you have in the building and so the higher that number, the correlation is a higher premium or not being able to find insurance,” said Valentina Gojcaj, who manages a portfolio of about 700 mostly rent-stabilized apartments in The Bronx and Manhattan.

Far Rockaway landlord Gary Schiller said insurance carriers may be operating under the belief that tenants with government rental assistance are less reliable.

“Maybe they feel … that these people don't take care of the apartment,” he said.

‘Legitimate concerns’ vs. discrimination

Insurance carriers have flexibility when it comes to what kind of properties they will cover. Many major carriers have recently pulled out of entire states, like Florida and California due to risks associated with climate change, such as flooding and wildfires. New York’s Department of Financial Services found that insurers have been losing money on property and casualty coverage for most of the last decade, most notably after Hurricane Sandy.

However, insurers may violate the law when they decline coverage based on tenant characteristics, DFS said.

Agency officials declined to speak on the record but referred to the agency’s report issued last year summarizing the rising cost of insurance and owners’ complaints of denials based on affordable and subsidized housing.

“In the process of fact-finding for this report, affordable housing owners indicated that insurance companies and producers often ask whether buildings contain affordable, subsidized, or Section 8 units, and what proportion of the buildings is comprised of such units, in order to make decisions about which properties to insure and at what price,” the report states.

DFS said New York law allows insurers to ask those questions if they are “reasonably related to actual or anticipated losses” but prohibits discrimination based on race, religion, gender disability and other protected classes.

“These insurer inquiries about affordable housing raise legitimate concerns from stakeholders about the potential for unfairly discriminatory results,” the agency added.

A spokesperson told Gothamist that in the coming weeks, the oversight agency will begin requesting more detailed information from carriers about whether they insure affordable housing, whether they ask about subsidized housing and how they use that information to determine their coverage decisions.

‘Every carrier's concerned about it’

Insurance carriers are supposed to make risk decisions based on actuarial calculations, according to state law. They use reams of data to determine whether they’ll lose money by insuring a property.

In its report, DFS said those decisions must be based on “sound underwriting practices and actuarial principles that are related to actual or reasonably anticipated loss experience.”

But it remains unclear what the actuarial reasoning is for questions about subsidized housing.

Brokers who spoke with Gothamist stopped short of saying there was a clear discriminatory intent in insurers’ decisions not to provide coverage.

Ian Sterling, a real estate program manager at the brokerage Bolton Street Programs, called subsidized housing denials “a very dangerous topic to be talking to people about” due to past litigation against carriers over the practice. Sterling said his company asks about subsidized housing to give insurance companies as much information as possible so that brokers don’t have to continuously request more documentation from building owners.

“The reason that we ask the question from a risk profile standpoint is that depending on the number of affordable housing units in a building, it may cause it to not be eligible,” Sterling said. “But if you wanted to know the rationale or the decision-making process behind that, you’d have to talk to the carriers.”

“Every carrier's concerned about it,” he added.

Few other companies would detail the reasons they require information about subsidized housing, or how that information factors into their decision-making.

Chaya Cooperberg, a spokesperson for the insurance carrier AmTrust, which insures some subsidized housing in New York City, said “low-income housing is one of many data points or considerations, such as building occupancy and loss history, that underwriters use in order to understand the full picture of a given risk.”

The term “loss history” refers to past claims payments at a property, such as settlements from a lawsuit or money issued to repair fire damage.

Other carriers have in the past explicitly excluded subsidized housing.

Underwriting guidelines issued by Travelers in 2007 ruled out “subsidized, public or government funded complexes” from its insurance coverage. Travelers removed that wording from its guidelines in 2015, according to court documents related to a Washington D.C. discrimination lawsuit

Multiple brokers and property owners interviewed by Gothamist speculated that one reason why insurers are more hesitant to provide coverage is a perception that tenants with housing vouchers are suing their landlords more often, leading to higher claims and payouts from insurance carriers.

However, a survey of 10 large affordable housing providers in The Bronx by the University Neighborhood Housing Program, or UNHP, found no evidence to back up that claim — or any “clear empirical basis” for the rising premiums or the denials.

“Throughout the portfolios included in our working group there are numerous buildings that have not had losses in a decade or more,” the organization wrote in its report issued last year. “This reality does not fit with the increased risk assessment we are hearing from brokers.”

UNHP is one of many property owners now urging state lawmakers to take action. A bill introduced last year would prohibit discrimination against affordable and subsidized housing by insurers.

Landlord Robert Lee, who rents to voucher recipients in his five Brooklyn buildings, is another.

He said his insurance premium went up by about 25% this year, and that his broker told him it was because he rents to subsidized tenants.

The rising rate is forcing owners to increase rents where possible, eliciting backlash from tenants and their advocates, he said.

“Landlords go for a 3% raise and [tenants ]want to shoot us. But this is one of the reasons why,” Lee said. “There are companies that are declining and they are raising their rates because no one is paying any attention to them.”

This story was updated to include comment from the insurance company Travelers.

StructValue([('url', 'https://gothamist.com/news/nyc-real-estate-firms-accused-of-housing-discrimination-face-sweeping-lawsuit'), ('title', 'NYC real estate firms accused of housing discrimination face sweeping lawsuit'), ('thumbnail', None)]) StructValue([('url', 'https://gothamist.com/news/new-yorkers-in-nycs-poorest-neighborhoods-face-higher-housing-discrimination-analysis-finds'), ('title', 'New Yorkers in NYC’s poorest neighborhoods face higher housing discrimination, analysis finds'), ('thumbnail', None)]) StructValue([('url', 'https://gothamist.com/news/plagued-by-staff-shortage-nyc-agency-fails-to-make-determinations-in-most-discrimination-cases'), ('title', 'Plagued by staff shortage, NYC agency fails to make determinations in most discrimination cases'), ('thumbnail', None)]) StructValue([('url', 'https://gothamist.com/news/ny-rep-nydia-vel%C3%A1zquez-takes-aim-at-landlords-fueling-us-housing-crisis'), ('title', 'NY Rep. Nydia Velázquez takes aim at landlords fueling US housing crisis'), ('thumbnail', None)]) StructValue([('url', 'https://gothamist.com/news/black-drivers-in-brooklyn-pay-more-for-car-insurance-analysis-finds'), ('title', 'Black drivers in Brooklyn pay more for car insurance, analysis finds'), ('thumbnail', None)])